Unlock the Power of Data: Transform Your Marketing Strategies with Data Science In the digital age, understanding the symbiosis between marketing and data science is not just an advantage; it's a necessity.

Unlock the Power of Data: Transform Your Marketing Strategies with Data Science In the digital age, understanding the symbiosis between marketing and data science is not just an advantage; it's a necessity.

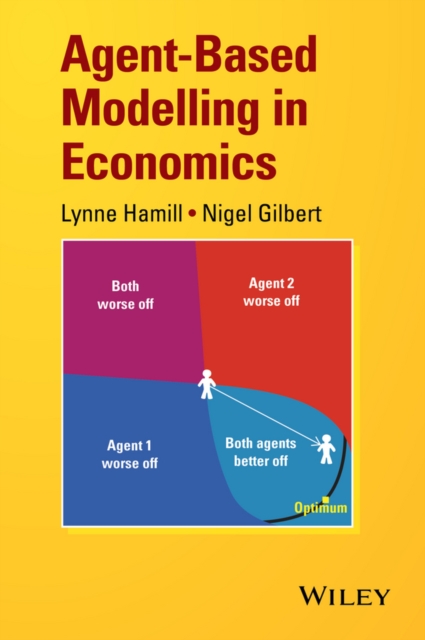

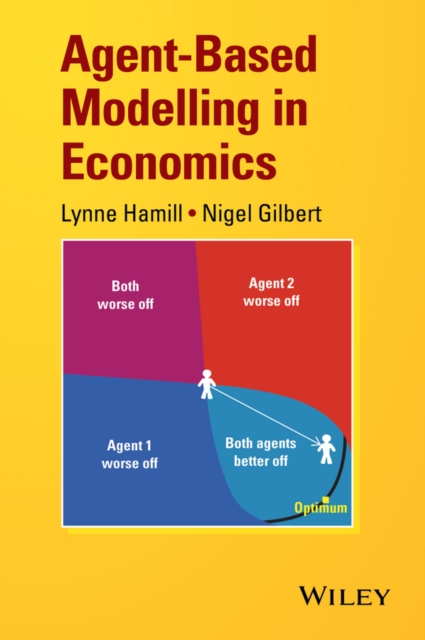

Agent-based modelling in economics Lynne Hamill and Nigel Gilbert, Centre for Research in Social Simulation (CRESS), University of Surrey, UK New methods of economic modelling have been sought as a result of the global economic downturn in 2008.

Agent-based modelling in economics Lynne Hamill and Nigel Gilbert, Centre for Research in Social Simulation (CRESS), University of Surrey, UK New methods of economic modelling have been sought as a result of the global economic downturn in 2008.

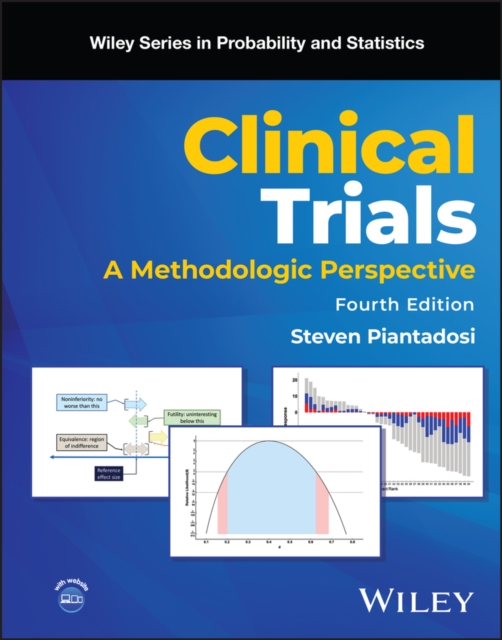

Comprehensive resource presenting methods essential in planning, designing, conducting, analyzing, and interpreting clinical trials The Fourth Edition of Clinical Trials builds on the text s reputation as a straightforward, detailed, and authoritative presentation of quantitative methods for clinical trials, discussing principles of design for various types of clinical trials and elements of planning the experiment, assembling a study cohort, assessing data, and reporting results.

Data Science Fundamentals with R, Python, and Open Data Introduction to essential concepts and techniques of the fundamentals of R and Python needed to start data science projects Organized with a strong focus on open data, Data Science Fundamentals with R, Python, and Open Data discusses concepts, techniques, tools, and first steps to carry out data science projects, with a focus on Python and RStudio, reflecting a clear industry trend emerging towards the integration of the two.

Comprehensive resource presenting methods essential in planning, designing, conducting, analyzing, and interpreting clinical trials The Fourth Edition of Clinical Trials builds on the text s reputation as a straightforward, detailed, and authoritative presentation of quantitative methods for clinical trials, discussing principles of design for various types of clinical trials and elements of planning the experiment, assembling a study cohort, assessing data, and reporting results.

A focused guide for healthcare simulation operations in education and training With the growing use of simulation within the field of healthcare, Healthcare Simulation: A Guide for Operations Specialists provides a much needed resource for developing the roles and responsibilities of simulation operations specialists.

Prospect, evaluate, purchase, and grow an existing business Buying a Business For Dummies guides you through the process of becoming an entrepreneur without starting from scratch.

The book is a collective work by a number of leading scientists, analysts, engineers, mathematicians and statisticians who have been working at the forefront of data analysis and related applications, arising from data science, operations research, engineering, machine learning or statistics.

Introduction to Statistical Analysis of Laboratory Data presents a detailed discussion of important statistical concepts and methods of data presentation and analysis Provides detailed discussions on statistical applications including a comprehensive package of statistical tools that are specific to the laboratory experiment process Introduces terminology used in many applications such as the interpretation of assay design and validation as well as fit for purpose procedures including real world examples Includes a rigorous review of statistical quality control procedures in laboratory methodologies and influences on capabilities Presents methodologies used in the areas such as method comparison procedures, limit and bias detection, outlier analysis and detecting sources of variation Analysis of robustness and ruggedness including multivariate influences on response are introduced to account for controllable/uncontrollable laboratory conditions

The book is a collective work by a number of leading scientists, analysts, engineers, mathematicians and statisticians who have been working at the forefront of data analysis and related applications, arising from data science, operations research, engineering, machine learning or statistics.

Ob Naturwissenschaftler, Mathematiker, Ingenieur oder Datenwissenschaftler - mit MATLAB haben Sie ein mächtiges Tool in der Hand, das Ihnen die Arbeit mit Ihren Daten erleichtert.

Introduction to Statistical Analysis of Laboratory Data presents a detailed discussion of important statistical concepts and methods of data presentation and analysis Provides detailed discussions on statistical applications including a comprehensive package of statistical tools that are specific to the laboratory experiment process Introduces terminology used in many applications such as the interpretation of assay design and validation as well as fit for purpose procedures including real world examples Includes a rigorous review of statistical quality control procedures in laboratory methodologies and influences on capabilities Presents methodologies used in the areas such as method comparison procedures, limit and bias detection, outlier analysis and detecting sources of variation Analysis of robustness and ruggedness including multivariate influences on response are introduced to account for controllable/uncontrollable laboratory conditions

Für Leser, die ein tiefes Verständnis der wissenschaftlichen Denkweise suchen, ist 'Wissenschaft und Hypothese' von Henri Poincaré ein unverzichtbares Werk.

'Nucleosynthesis in thin layers' develops a unified theory of five interactions within a fractal universe based on information-currents from an algebraic algorithmic point of view.

Prospect, evaluate, purchase, and grow an existing business Buying a Business For Dummies guides you through the process of becoming an entrepreneur without starting from scratch.

SHORTLISTED FOR THE ROYAL SOCIETY TRIVEDI SCIENCE BOOK PRIZE 2024 'Fascinating, witty and perspective-shifting' Oliver Burkeman'A remarkable book about a remarkable theorem' Will Storr'Witty, lively and best of all, extremely nerdy.

Install data analytics into your brain with this comprehensive introduction Data Analytics & Visualization All-in-One For Dummies collects the essential information on mining, organizing, and communicating data, all in one place.

A Tangled Tale is a collection of ten brief humorous stories by Lewis Carroll (Charles Lutwidge Dodgson), published serially between April 1880 and March 1885 in The Monthly Packet magazine.